Insights and Updates

.png)

AI In Credit: Risks You Can't Ignore

The risks of AI in credit management are real. Here are practical strategies for protecting your B2B team from the most common AI pitfalls and failure modes.

What Are the Biggest Risks of Using AI in Credit?

AI is already transforming how credit teams work. Automating credit applications, analyzing risk data, monitoring accounts in real time — these capabilities are table stakes now, not experiments.

The challenge isn't whether to use AI. It's how to use it without getting burned.

In partnership with the National Association of Credit Management (NACM), our team at Credit Pulse developed a two-part webinar series on AI in Credit. The goal was to help credit professionals cut through the hype and focus on where artificial intelligence truly adds value — and where the human element still matters most.

👉 View our free “AI in Credit: Risks You Can’t Ignore” webinar on NACM

Understanding the Real Risks

AI delivers faster insights, improves consistency, and automates repetitive work. When it fails, it fails loudly. Across industries, three failure patterns keep showing up:

- Hallucinations: AI delivers confident but incorrect information.

- Bias and Incomplete Data: The system learns from partial or skewed data.

- Over-Automation: Machine logic replaces human judgment.

None of these failures make AI unsafe. They make it a tool that demands discipline, context, and ongoing validation.

AI Hallucinations: When Confidence Turns Into Error

A hallucination happens when AI generates something that sounds right but has no basis in fact. In credit, that can look like a financial summary with fabricated numbers, an incorrect recommendation, or a risk analysis that ignores key context.

Hallucinations fall into four categories:

- Factual: The data itself is wrong or fabricated.

- Contextual: The system misreads the customer environment.

- Logical: The reasoning is flawed, even if the inputs are valid.

- Multimodal: The AI misinterprets data from multiple sources, such as text and documents.

These mistakes happen because AI models are designed to predict the most likely answer, not the most accurate one. When data is thin, the model fills in the blanks instead of flagging the gap.

For a deeper look at this issue, visit our feature: AI Hallucinations in Credit Automation.

Bias and Incomplete Data: What the Model Misses

AI is only as good as the information it’s trained on. It can’t use intuition to fill gaps. A model relying only on static scores or limited financials will miss important context.

Imagine a customer with strong financials but a new lien filed last week. The model might extend credit confidently without catching that update. Or consider a small business with a thin credit file but excellent trade performance and cash flow — the system could decline it for lack of data.

In both cases, the model isn’t wrong in a technical sense. It’s incomplete. That’s why human oversight remains essential.

Over-Automation: When Speed Becomes a Liability

Automation saves time, but too much automation creates risk. When systems make credit decisions without human review, small model errors compound fast.

Over-automation shows up two ways:

- Over-Extending: The AI approves too much credit because it misses new warning signs.

- Under-Extending: The AI rejects good customers because it lacks alternative data.

Automation should make credit professionals faster, not replace them. Let AI handle structured, repeatable tasks. Keep humans on context and exceptions.

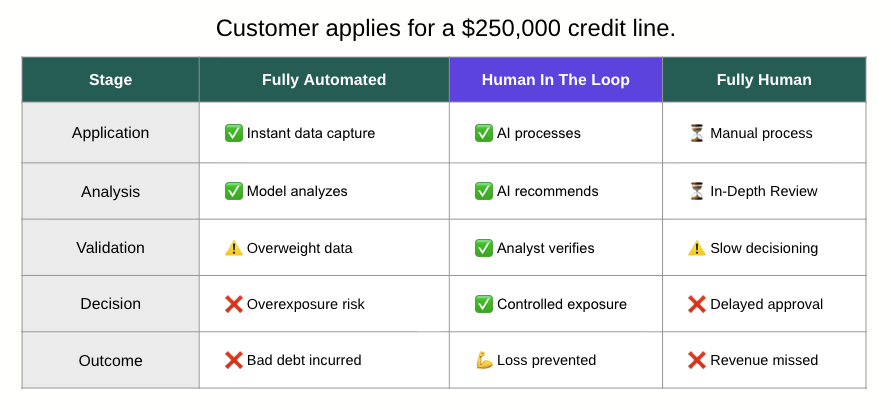

The Human in the Loop Advantage

High-performing credit teams use AI to inform decisions, not make them entirely. A human-in-the-loop approach blends automation with oversight — speed without sacrificing control.

When AI and humans work together, credit teams prevent losses while still hitting growth targets.

Keeping AI Honest

Responsible AI starts with structure and transparency. Every system that influences credit decisions needs controls to explain, audit, and improve its results.

Four proven approaches:

1. Data Quality

Reliable AI starts with clean data.

- Clean and verify data sources before adding them to your model.

- Cross-check critical information regularly.

- Flag low-confidence extractions and require review.

- Schedule monthly data audits and discrepancy alerts.

Result: Better data leads to more accurate and balanced outcomes.

2. Audit Trails

Transparency builds trust. Every action your AI system takes should be traceable.

- Log and timestamp each AI recommendation.

- Record when humans override a decision.

- Make every action explainable to non-technical stakeholders.

Result: Visibility into how and why decisions are made.

3. Governance

AI must operate within policy boundaries.

- Define what can and cannot be automated.

- Make human overrides simple and accessible.

- Review rules regularly to confirm alignment with credit policy.

Result: Human control stays central to every automated decision.

4. User Feedback

AI should evolve with your business.

- Create feedback loops for continuous learning.

- Track model performance and accuracy.

- Host regular review sessions to challenge outputs.

Result: Models improve with real-world use and human input.

Balancing Speed and Judgment

AI in credit delivers better decision-making, not just faster processing. That only works when teams use automation with context, clarity, and accountability.

The right mix of human oversight and machine intelligence keeps credit management both efficient and responsible. AI should enhance expertise, not replace it.

The Credit Pulse Approach

At Credit Pulse, transparency, governance, and data quality define how we build. Our platform uses explainable models, reason codes, and traceable audit trails that keep humans in control of every outcome.

AI works for credit professionals — not the other way around. With the right structure, teams can prevent bias, reduce bad debt, and move confidently into digital credit.

Frequently Asked Questions

What is model bias in credit AI and why does it matter?

Model bias occurs when an AI system systematically disadvantages certain groups because of patterns in its training data. In credit, this can mean unfairly denying credit to businesses in certain geographies or industries—creating legal and reputational risk.

How can I ensure AI credit decisions are explainable?

Choose platforms that offer explainability features—showing which factors drove a decision and by how much. Maintain human review for borderline cases. Document your model governance process to satisfy auditors and regulators.

What happens when an AI credit model is wrong?

Errors can manifest as false approvals (extending credit to customers who default) or false denials (blocking creditworthy customers). Both are costly. Regular model validation, performance tracking, and human override capabilities are essential safeguards.

Are there regulations governing AI use in credit decisions?

Yes. In the US, credit decisions must comply with the Equal Credit Opportunity Act (ECOA) and Fair Credit Reporting Act (FCRA), which require adverse action notices and prohibition on discriminatory factors. B2B credit has more flexibility than consumer credit but is not exempt from scrutiny.

How do I reduce over-reliance on AI in credit management?

Set clear thresholds for human review of borderline scores, monitor model drift regularly, and maintain staff capability to make decisions without the tool. Treat AI as a decision-support system, not a replacement for credit judgment.

.png)

.png)

.png)

Transform your credit process today.

Meet with our team or try us free for 30 days.