Insights and Updates

The Power of Alternative Data in Credit Risk Management

Discover how alternative data gives credit teams deeper insights, predicts risk earlier, and fills gaps traditional credit reports leave behind.

Alternative data in trade credit refers to non-traditional data sources—such as bank transaction data, utility payments, real-time trade payment networks, and online business signals—used to supplement or replace conventional credit bureau information in credit assessments. Traditional credit data only tells half the story. That's why so many finance teams get blindsided by bankruptcies, fraud, and bad debt — even when the credit score looked fine.

At Credit Pulse, we've built a platform that combines traditional credit data with alternative data, AI-driven models, and predictive insights — so credit teams see risk coming before it hits.

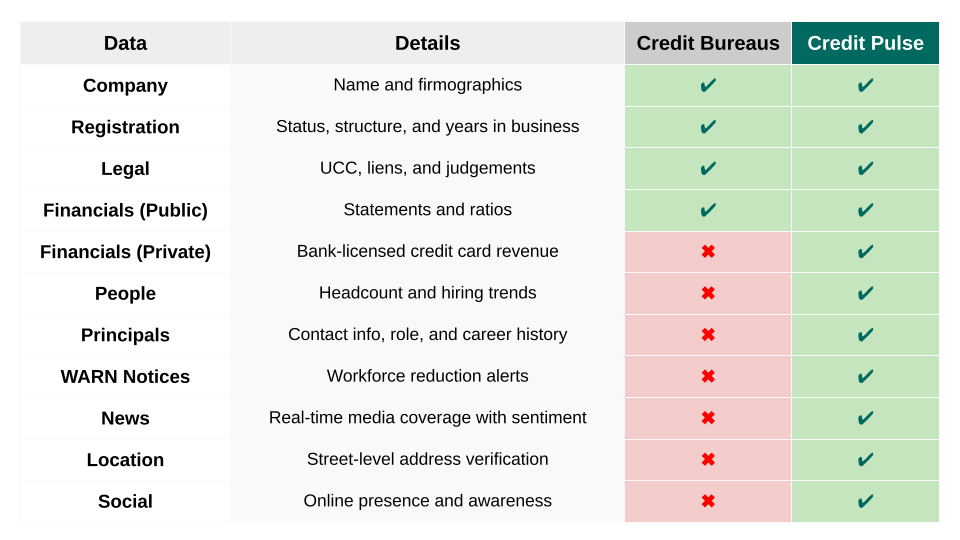

Why Traditional Data Falls Short

Most bureaus stick to trade lines, registrations, and public financials. Useful, but incomplete. They miss today's most predictive signals:

- Executive exits and leadership changes

- Hiring freezes or WARN notices

- Legal filings and lawsuits

- Negative press coverage

- Private revenue and transaction trends

Without these, you're making credit decisions with only a fraction of the picture.

Why Alternative Data Matters

- Traditional data shows where a company's been.

- Alternative data shows where it's going.

Signals like layoffs, leadership turnover, lawsuits, and hiring trends often surface risk months before it shows up in payment behavior or financial statements. For private companies, this may be the only forward-looking window you have.

Key Alternative Data Signals Credit Pulse Tracks

👥 People Analytics

Executive exits, layoffs, and WARN notices reveal stress before it hits the balance sheet.

- C-suite changes

- Hiring spikes or freezes

- Workforce reductions

Shrinking teams = red flag. Growing teams = green light.

💳 Private Financials

Most small businesses don't share timely financial statements. Credit Pulse closes the gap with:

- Annual revenue trends

- B2C card transaction volume

- Payment acceptance activity

This gives credit teams a near real-time view of financial health.

👨💼 Principals & Leadership Data

A company is only as strong as its leaders. We track:

- Executive tenure and turnover

- Verified contact info

- Current vs. past roles

- Linked professional profiles

Stable leadership boosts confidence. High turnover signals risk.

🌐 Digital Presence & Web Signals

Online visibility reflects credibility. Red flags include:

- Dead websites

- Dropping site traffic

- Inactive LinkedIn or job boards

If a company disappears online, risk is rising.

📰 News & Media

Adverse news often predicts financial distress. We monitor:

- Lawsuits and regulatory actions

- Data breaches and scandals

- Positive press (funding, awards, expansion)

- Sentiment trends by sector

News is data — good or bad, it shifts risk exposure fast.

The Results: 7x More Accurate Predictions

Credit Pulse predicts 7x more bankruptcies than leading bureaus, especially in small and private companies that others miss. That accuracy means:

- Fewer write-offs

- Reduced fraud exposure

- Faster, smarter credit approvals

For many customers, avoiding just one missed bankruptcy pays for the platform.

The Bottom Line

Trade credit decisions can't rely on outdated reports alone. By combining traditional and alternative data, credit teams get a 360° view of customer health — spotting risks earlier, approving faster, and protecting revenue.

Credit Pulse helps finance leaders modernize credit risk management with AI-driven monitoring, alternative data, and predictive insights.

Frequently Asked Questions

What types of alternative data are used in trade credit decisions?

Common alternative data sources include bank account transaction data, real-time trade payment networks (like the Dun & Bradstreet Trade Exchange), utility and telecom payment history, e-commerce transaction data, and web/digital signals such as website age and online reviews.

When is alternative data most valuable?

Alternative data is most valuable when bureau data is thin—for newer businesses, foreign entities with limited US credit history, or sole proprietors whose personal and business credit are intertwined. It fills gaps that traditional scores can't address.

How reliable is alternative data compared to bureau data?

Quality varies by source. Bank transaction data and structured payment network data are highly reliable. Unstructured signals (social media, reviews) carry more noise. The best credit models blend traditional bureau scores with vetted alternative data sources.

Does using alternative data raise compliance concerns?

Yes. Data must be sourced ethically, with proper consent mechanisms where required. Under FCRA guidelines for consumer-adjacent decisions, permissible purpose and dispute rights apply. B2B credit has more latitude, but data governance policies are still important.

How do I start incorporating alternative data into my credit process?

Start with one or two high-signal sources—such as a real-time trade payment network or bank data feed—and measure lift over your existing model. Work with your credit platform vendor to integrate these sources without disrupting existing workflows.

Transform your credit process today.

Meet with our team or try us free for 30 days.