Insights and Updates

.png)

Bertucci's Bankruptcy: What Happened?

A breakdown of how Bertucci's Italian restaurant chain filed for bankruptcy three times and what drove its long decline.

Some brands collapse in a blaze. Others fade slowly until there is nothing left. Bertucci’s, once a beloved Northeast pizza chain, is a clear example of how slow strategic failure, market shifts, and financial pressure can eventually sink even the strongest reputations.

In April 2025, Bertucci’s filed for Chapter 11 bankruptcy for the third time, leading to immediate restaurant closures across Massachusetts and Rhode Island.

Here’s a full breakdown of how we got here and what credit leaders should take away.

Background

Bertucci’s was founded in 1981 in Somerville, Massachusetts, built around a signature experience: authentic brick-oven pizza served in a cozy, family-style setting.

The formula worked. By the late 1990s, Bertucci’s was a regional powerhouse, popular across New England and the Mid-Atlantic.

But while Bertucci’s stayed true to its traditional model, the restaurant landscape shifted around it. Fast-casual dining grew, malls lost foot traffic, and customer expectations evolved. Bertucci’s struggled to evolve with them.

Timeline of Trouble

Bertucci’s decline played out over two decades, with key milestones marking its fall:

- 1998–2006: Ownership changes multiple times. Leadership instability begins affecting operations.

- 2010–2017: The rise of fast-casual competitors like Panera and Chipotle cuts into Bertucci’s customer base.

- 2018: First Chapter 11 bankruptcy. Closes dozens of underperforming locations. Acquired by Earl Enterprises.

- 2022: Second Chapter 11 bankruptcy. Bertucci’s cites rising labor costs, food inflation, and pandemic impacts.

- April 2025: Third Chapter 11 bankruptcy filed. Several restaurants immediately closed in Massachusetts and Rhode Island.

Each filing offered a chance for a reset. But without deeper changes to its model, Bertucci’s kept slipping backward.

The Warning Signs Were There

The warning signs ahead of Bertucci’s 2025 bankruptcy were easy to spot — if you were watching the data.

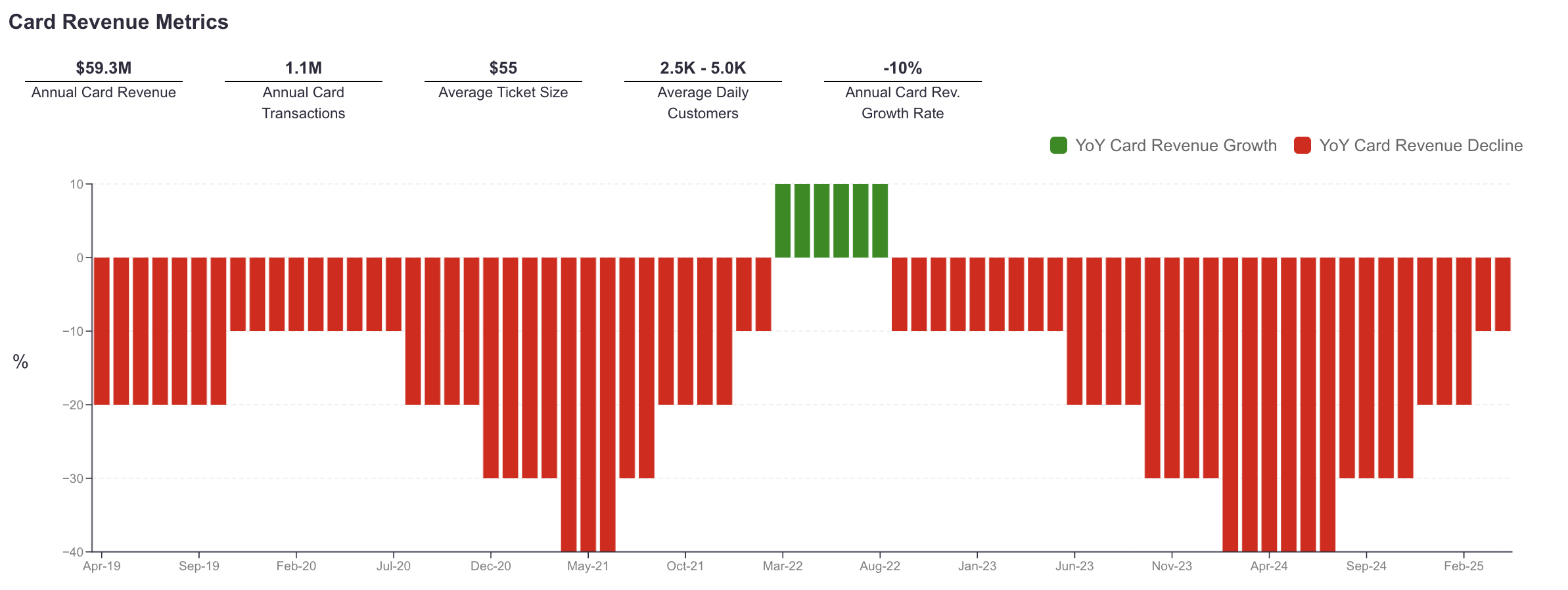

Revenue Decline

- Annual card revenue shrank to $59.3M with a negative 10% year-over-year growth rate.

- Revenue was negative for most periods since 2019, with only a brief recovery in early 2022.

Weakened Customer Traffic

- Average daily customer count hovered between 2,500 and 5,000, below earlier years' benchmarks.

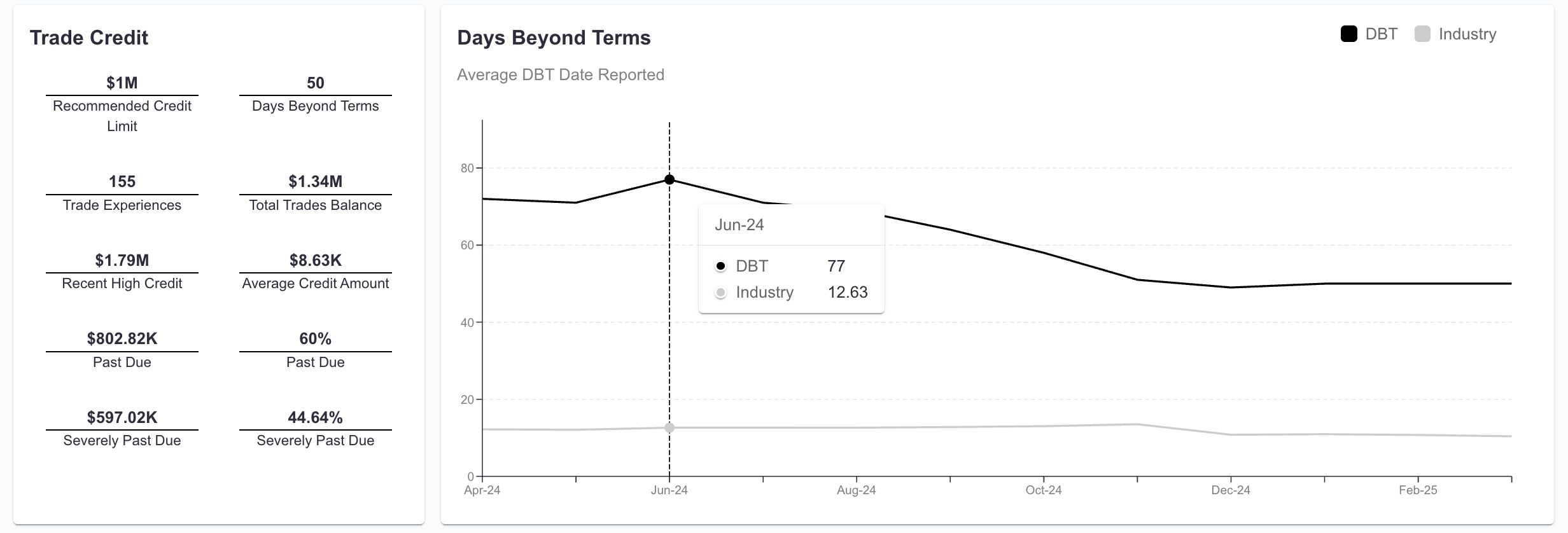

Credit Deterioration

- Days Beyond Terms (DBT) climbed as high as 75 days in 2024 before modestly improving to 50 days in early 2025, still far worse than the industry average.

- 60% of Bertucci’s trade balances were past due, with nearly 45% severely delinquent.

- Trade balances outstanding grew heavier in the 91+ days overdue category, showing strained liquidity.

Headcount Erosion

- After peaking near 950 employees in 2015, Bertucci’s workforce steadily declined year over year.

- As of early 2025, headcount was below 400 employees, a 2.9% drop over the last 12 months alone.

Payment Behavior Stress

- Outstanding trade lines showed a growing share of invoices slipping past 91+ days overdue.

- Despite a $1M recommended credit limit, Bertucci’s outstanding and aging trade behavior told a story of mounting pressure that was unsustainable.

Bertucci’s financial health was declining across every key dimension long before bankruptcy became public.

Lessons for Credit and Risk Professionals

Bertucci’s offers an important reminder: A slow decline can be just as fatal as a sudden collapse.

Multiple bankruptcies are a major risk flag. Emerging from bankruptcy without structural change often leads to repeated failures.

Revenue rebounds must be sustainable. A brief spike in 2022 did not reflect real recovery. Fundamental problems remained unaddressed.

Worsening payment behavior is an early alarm. Ballooning DBT, a rising share of severely overdue invoices, and shrinking employee counts were clear signs of deep trouble.

Adaptation is non-negotiable. Businesses that fail to meet shifting customer expectations eventually lose relevance, no matter how strong they once were.

Credit Pulse: Catch the Early Signals

At Credit Pulse, we track early signals that traditional reports miss. From falling headcounts to deteriorating payment behavior, we identify risk before it becomes a crisis.

Bertucci’s third bankruptcy was not surprising for those who were watching the right indicators. You can stay ahead of situations like this too — before they reach your balance sheet.

Want to learn how? Let's talk.

Transform your credit process today.

Meet with our team or try us free for 30 days.