Insights and Updates

Harvest Sherwood Food Distributors Bankruptcy

How customer concentration and operational frailties drove Harvest Sherwood Food Distributors into Chapter 11 — and what B2B credit teams should learn.

When a company with around $4 billion in annual revenue files for Chapter 11 in just a matter of weeks, one fact jumps out: scale alone is not a safeguard. Harvest Sherwood Food Distributors, Inc. (HSFD) provides a textbook case of how a dominant player in wholesale food distribution imploded. What happened? How did a major distributor become financially incapable almost overnight? The answers matter, especially for credit teams, suppliers, risk managers and sales executives working with high-volume, low-margin distributors.

What Was Harvest Sherwood?

Harvest Sherwood emerged from the merger of legacy regional players to become the largest independent food distributor in the U.S. At its peak it:

- Operated multiple distribution centers servicing grocery chains, restaurants and other foodservice operators.

- Handled meat, poultry, seafood, and bakery products with its own fleet logistics and cold-chain capabilities.

- Reported revenues around $4 billion, affirming its scale and presence in the perishables supply chain.

This set the stage for a large business, but also for significant risk, as we’ll see.

How They Managed Credit, Operations & Supply-Chain Risk

In theory, HSFD’s business model required:

- High inventory turnover and tight margins. Perishables demand swift movement, accurate forecasting and minimal spoilage.

- Strong vendor payables and receivables management. Suppliers expect prompt payment. Customers expect consistent fufillment. Any disruption ripples.

- Minimal customer concentration risk. Losing a large customer or major contract can destabilize the cash-flow model quickly.

- Operational systems that deliver real-time visibility into inventory, logistics and demand across multiple sites. Without this, structural weaknesses build.

From available reports, HSFD appeared to struggle in several of these areas.

Key Red-Flags & Signals That Should Have Been Visible

1. Dependence on a major customer relationship

HSFD alleged that one of its largest customers, Sprouts Farmers Market, informed HSFD in December 2024 that it would transition to self-distribution. HSFD claims that this decision led to an unresolved receivable of about $41.8 million and left HSFD with approximately $25 million in excess inventory (tray-pack chicken) when Sprouts stopped placing orders. Once a distributor becomes critically dependent on one anchor customer, the risk of that customer changing strategy becomes existential.

2. Credit rating & vendor alarms

In early 2025 HSFD was downgraded by credit rating agencies (e.g., from “Recommended” to “Cautionary”), which triggered tighter terms from suppliers and decreased liquidity flexibility. Without vendor trust, payment terms worsen and operational stress builds.

3. Operational / structural deficits

Reports indicate HSFD had a patchwork of legacy systems post-merger, limited integration of demand-planning and ERP systems, and internal silos across distribution centers. When you combine that with the perishables business model, even moderate disruptions become amplified.

4. Rapid escalation & liquidity crunch

HSFD ceased operations around April 21, 2025, laid off roughly 1,500 employees and filed for Chapter 11 on May 5, 2025. At the time of filing it listed liabilities estimated between $323.5 million to $558.5 million. The rapid timeline signals that catastrophic failure was not just based on one event—but revealed long-standing fragility.

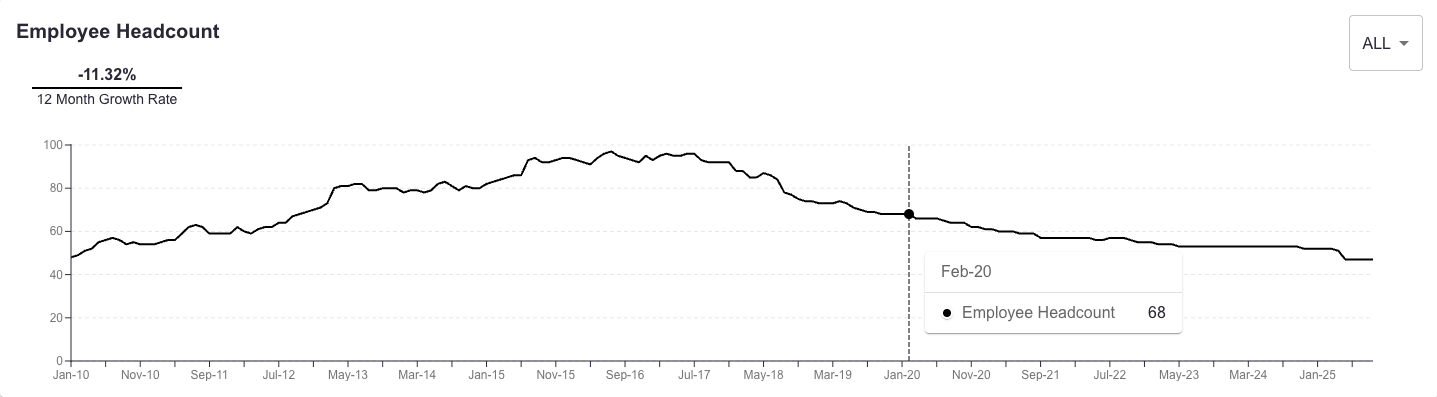

The signals became apparent years ago for those watching company operations. Employee count has been dwindling before 2020.

HFSD Bankruptcy Timeline

- December 2024: Sprouts signals move to self-distribution for certain product lines.

- February 2025: Sprouts stops placing tray-pack chicken orders; HSFD faces excess inventory and receivables stress.

- April 2025: HSFD shuts down wholesale operations; mass layoffs across multiple sites.

- May 2025: HSFD and affiliated entities file for Chapter 11 bankruptcy in Northern District of Texas (Case No. 25-80109)

- May 2025: Court approves access to roughly $104 million of debtor-in-possession financing to wind down operations.

Why This Matters for Credit, Sales & Risk Teams

- Customer concentration = credit ticking time-bomb. If you’re evaluating a distributor, ask: What percentage of their revenue comes from their top 5 customers? Are any of those customers signaling a strategy shift?

- Operational visibility is a credit vector. Credit risk is not just about past due receivables. it’s about inventory health, vendor payment terms, forecasting accuracy and customer demand stability.

- Supplier trust matters. Once key vendors perceive risk of non-payment, they shorten terms or halt supply, triggering further operational decline.

- Scale without flexibility is brittle. Large distributors can still collapse swiftly if they lack agility, diversified customers and resilient cash-flow models.

- Use collapses as teaching tools. Share the Harvest Sherwood case in risk-training, vendor/supplier outreach and sales positioning to underline the importance of early warning signals.

Lessons & Takeaways

- Do not assume size equals stability. HSFD had billions in revenue—but millions in uncollected receivables and weak operational foundations.

- Monitor top-customer behavior. A major client’s exit or change in strategy can cascade through a distributor’s entire value chain.

- Build discipline around vendor and cash-flow monitoring. Suppliers pulling back is a red-flag for liquidity issues.

- Prioritize system integration, data transparency and forecasting in business models that depend on perishable goods.

- For credit teams: ask operational as well as financial questions. Inventory gluts, sudden vendor term changes, and customer cancellation patterns all signal elevated risk before the financials show up.

FAQ

Q: Could HSFD have been saved?

A: Possibly, if the company had earlier diversified its customer base, strengthened its forecasting and mitigation around a major customer exit, and had stronger vendor/receivable buffers. But once the liquidity bleed began and vendor trust eroded, the window closed.

Q: What does this mean for suppliers to distributors?

A: Always monitor the credit health of the distributors you rely on. Especially if they supply major chains or high-volume customers. If you see signals like large overdue receivables, customer contract shifts, or vendor payment delays—consider tightening your exposure.

Q: What should credit risk platforms focus on going forward?

A: Platforms should incorporate operational signals: customer contract shifts, inventory levels (especially perishables), vendor payment behavior, and customer concentration metrics. Not just traditional financial ratios.

Closing Thoughts

The demise of Harvest Sherwood is not only a cautionary tale of one distributor failing, but a case study in how structural weaknesses, customer reliance, operational inflexibility and credit risk interplay in a high-volume, low-margin industry. For credit teams, suppliers and distributors alike, the lessons are clear: sense the shifting ground early, don’t assume scale insulates you, and integrate operational risk into your credit lens.

Were You Impacted?

If your company has been impacted, check out our resource guide for tips and best practices of what to do next: "My Customer Went Bankrupt—Now, What?"

Want to see how we catch these signs before it’s too late? Try Credit Pulse free for 30 days →

.png)

Transform your credit process today.

Meet with our team or try us free for 30 days.