Insights and Updates

.png)

Is Peloton Heading for Bankruptcy?

An analysis of Peloton's financial struggles, declining momentum, and whether the company is at risk of filing for bankruptcy.

Peloton Interactive, Inc. (NASDAQ: PTON) once led the at-home fitness revolution.

Today, the company is struggling with shrinking revenues, heavy debt, leadership turnover, and major operational challenges — all classic warning signs that bankruptcy could loom ahead.

Here's what we know: Falling consumer demand, persistent cash burn, and weakening operational trends have pushed Peloton into high bankruptcy risk territory.

Timeline of Trouble

Here's a look at key events shaping Peloton’s downfall:

- 2020–2021: Pandemic boom. Revenue and subscribers surge. Stock price peaks at $160+ per share.

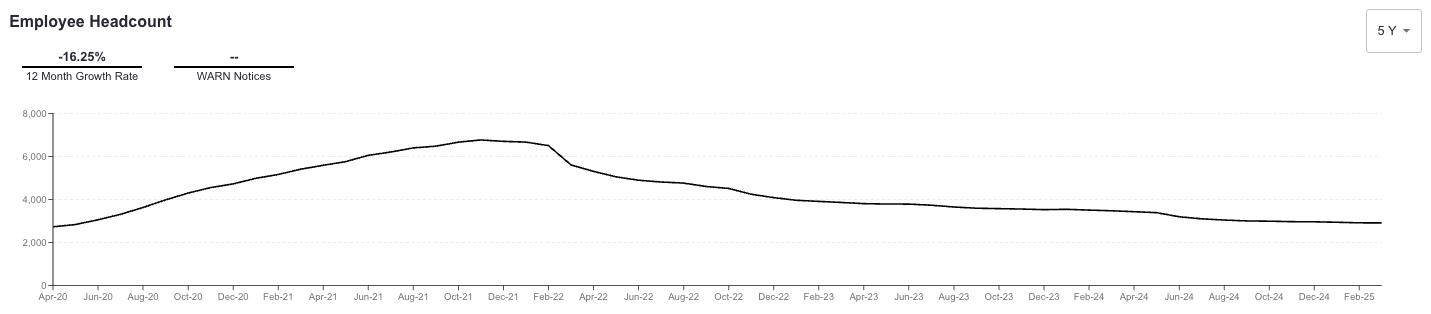

- 2021: Headcount reaches nearly 8,000 employees.

- Late 2021: Growth stalls as gyms reopen; inventory piles up.

- Feb 2022: CEO John Foley resigns; Barry McCarthy (ex-Netflix/Spotify CFO) steps in.

- 2022: Peloton cuts 2,800+ jobs (~20% of workforce).

- Aug 2022: Posts $1.24B loss; starts selling equipment on Amazon.

- Early 2023: Stock declines; shifts to "asset-light" model, outsourcing manufacturing.

- May 2024: McCarthy resigns; 15% workforce cut (~400 more jobs).

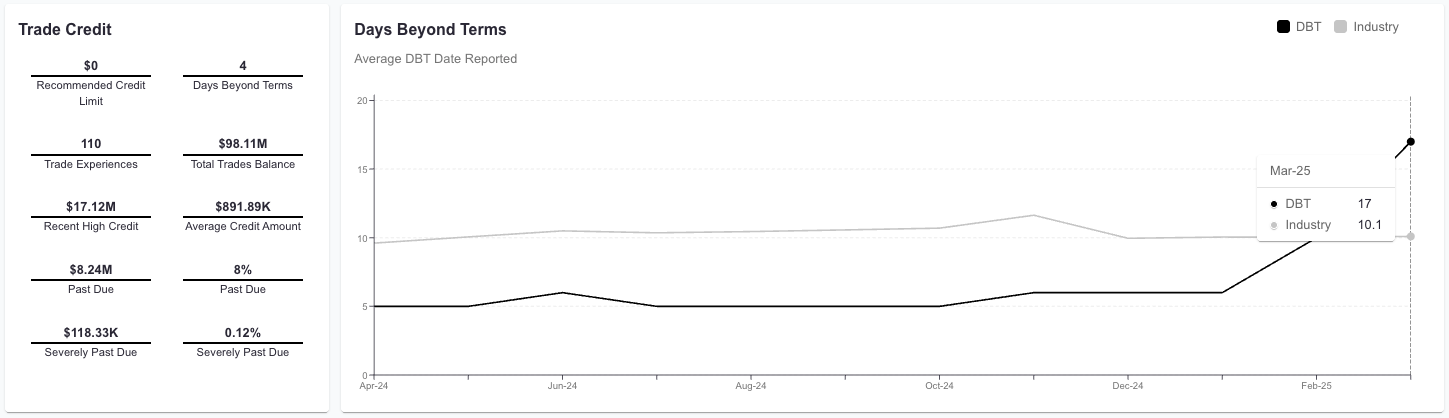

- March–April 2025: Headcount down 16% year-over-year, DBT rises to 17 days (vs. 10.1 industry avg).

- 2025: Stock trades below $4 with a minor recent rebound to $6.

Cracks in the Foundation

The company has an Altman Z-Score of -1.71, which suggests a significant risk of bankruptcy within the next two years. And several major distress signals are flashing red for Peloton:

Revenue Collapse

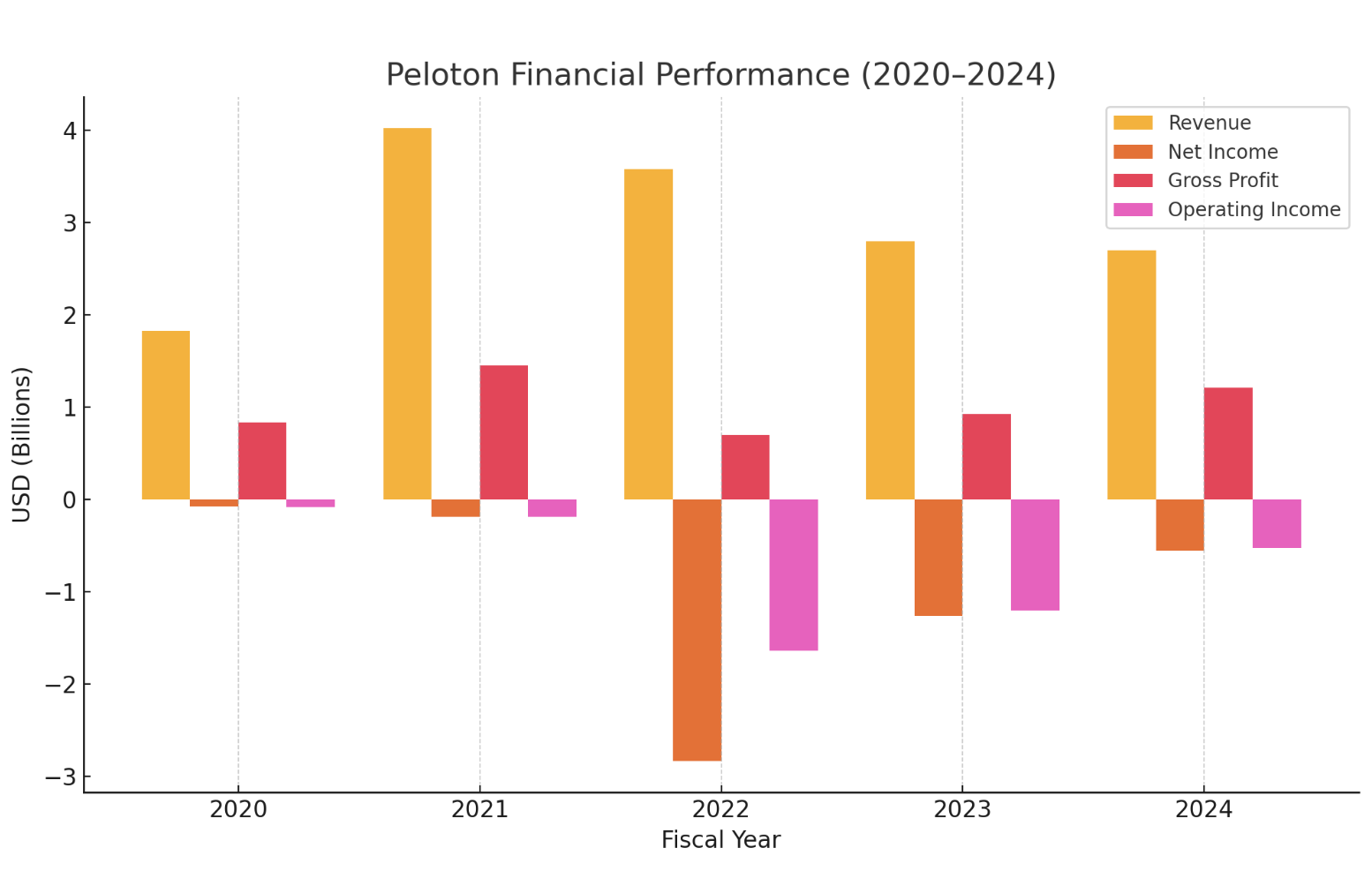

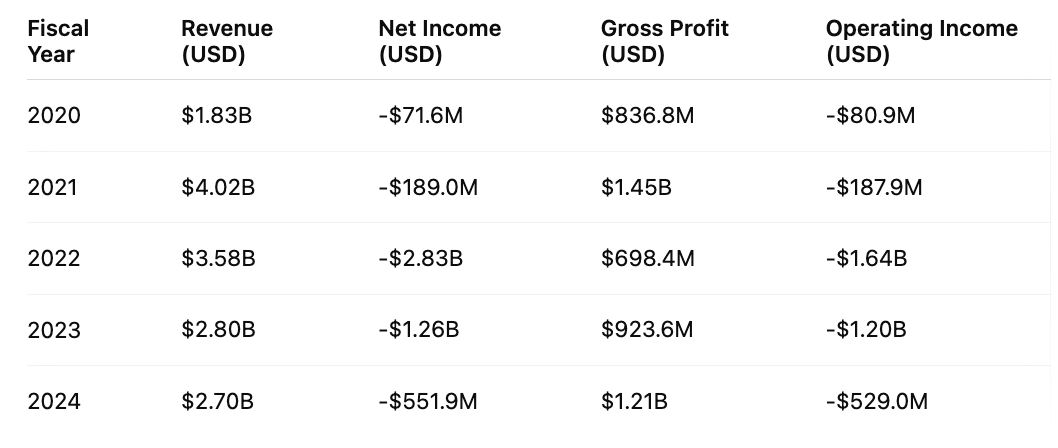

Peloton skyrocketed in 2021 to over $4 billion in revenue during the pandemic boom. Since then, revenue has steadily declined each year, falling to around $2.7 billion in 2024. The takeaway is clear: the COVID-driven surge was not sustainable, and Peloton has struggled to build a strong enough growth engine for the post-pandemic market.

Volatile Stock Markets—Shifting Up?

Peloton’s stock price has fallen over 90% from its pandemic peak, reflecting a collapse in investor confidence as revenue shrinks and profitability remains elusive. Despite a recent small rebound and a new analyst "buy" rating, the stock still signals high risk and uncertainty about the company's long-term survival.

Shifting Credit Profile

Peloton’s credit profile is beginning to shift. Historically, only a small portion of trade balances became past due, but that trend is changing. Currently, 8% of trade balances are past due, representing over $8.24 million in outstanding overdue amounts. This rise in delinquencies signals growing strain on Peloton’s ability to meet its short-term obligations.

Shrinking Workforce

Peloton’s employee headcount has declined sharply from its 2021 peak, with a 16% year-over-year drop. Leadership turnover at the CEO level has further destabilized morale and clouded the company's long-term vision, compounding internal challenges during a critical period of restructuring.

Familiar Distress Signals

The signs are alarmingly similar to other consumer brands that collapsed after rapid rises:

- Overexpansion during a boom without sustainable long-term demand.

- Leadership instability just as financial pressures hit.

- Late payments and strained vendor relationships.

- Revenue dependency on an outdated model without successful reinvention.

This echoes the downfall patterns of companies like GoPro and FitBit.

So, What Happens Next?

Peloton faces a narrow — but not impossible — path forward.

While a recent buy rating from analysts signals cautious optimism around a potential turnaround, the company’s fundamentals remain strained. Without a dramatic operational rebound or strategic acquisition, bankruptcy or an out-of-court restructuring remains a real risk over the next 12–24 months.

Private equity interest could still materialize, particularly for Peloton’s strong brand and subscriber base, but valuation erosion and sustained cash burn limit its options. Vendor tightening, rising competition, and customer churn continue to apply pressure making the next 1–2 years a critical window to either stabilize or spiral further.

Proactive Credit Strategies

Lessons from Peloton’s situation:

- Tighten credit on companies showing late payment or falling revenue signals early.

- Monitor leadership turnover as an early sign of internal instability.

- Watch for industry shifts that undermine once-thriving demand models.

- Use real-time payment behavior tracking to stay ahead of financial distress.

If your credit policies don’t catch risks like Peloton’s early, it may be time to rethink them.

.png)

Transform your credit process today.

Meet with our team or try us free for 30 days.