Insights and Updates

.png)

First Brands Group Bankruptcy: What Happened?

First Brands Group — parent of FRAM, TRICO, ANCO, and Autolite — filed Chapter 11 in Texas in 2025. Here's what happened and what credit teams should learn.

First Brands Group is a large aftermarket auto parts roll-up that owns or licenses well-known lines: FRAM, Luber-finer, TRICO, ANCO, Autolite, Raybestos, Centric, StopTech, Carter, StrongArm, Reese, Draw-Tite, Tekonsha, Fulton, and more. This matters because these are high-velocity maintenance categories that feed retailers, distributors, and service chains

The Filing: Dates, Venue, Advisors, and Money

- Venue: Southern District of Texas. International ops stay out of U.S. cases and are expected to continue. Business Wire

- DIP financing: $1.1B from an ad hoc group of cross-holders to fund payroll, vendors, and working capital while the company restructures. Business Wire

- Advisors: Weil, Gotshal & Manges (debtor counsel), Lazard (IB), Alvarez & Marsal (FA). Communications by C Street. Lenders advised by Gibson Dunn and Evercore. Business Wire

Why it matters: Size, complexity, and ubiquity of the brands make this one of the marquee 2025 filings. It will set precedents on supply-chain finance transparency and off-balance-sheet risk. Bloomberg

The Bomb Under the Floorboards: Off-Balance-Sheet Financing

Court disclosures and reporting say a special committee is probing whether customer invoices were pledged more than once across receivables-financing programs. Think “double-pledging” or commingled collateral across factoring lines and inventory loans. Reported figures cite:

- $11.6B total liabilities, $9.3B “core” debt excluding factoring, potential $2.3B receivables shortfall tied to factoring, and $376M of inventory collateral implicated. Reuters

Financial press also flags lenders seizing working capital, and concerns that inventory collateral moved beyond lender reach, which escalated the rush to Chapter 11. Financial Times+1

Translation: If documents confirm the receivable reuse or collateral mix-ups, lien priority and recovery math get messy fast.

How We Got Here: The Strategy That Stopped Working

- Roll-up growth + leverage. Years of acquisitions built a big catalog but also layered complex debt. The Wall Street Journal

- Heavy reliance on receivables and inventory finance. Cheap in good times, painful in a credit squeeze. The Wall Street Journal

- Transparency demands from lenders. Attempted refinancings reportedly stalled when lenders pushed for quality-of-earnings and clear views into supply-chain finance. Confidence eroded. The Wall Street Journal

- Liquidity stress → defaults → cash grabs. A reported $27M cash seizure by a bank, low cash on hand, and tumbling loan prices accelerated the filing. Financial Times

What It Means For…

Distributors and Retailers

Expect business-as-usual during Chapter 11 thanks to the $1.1B DIP, but plan for tight allocations and pricing volatility if suppliers or logistics tighten. Map substitutes across filtration, brakes, wipers, and towing catalogs now. Business Wire

Competitors

Window to grab shelf space and program business if First Brands trims SKUs, rationalizes channels, or sells assets. Monitor court motions for any §363 sales of product lines or IP. (Common in large parts cases.)

Employees and Vendors

Employees are usually protected on wages and benefits via first-day orders. Vendors supplying post-petition are “administrative” and should be paid. Pre-petition trade is likely impaired and becomes part of a plan recovery. Business Wire

Creditors

Priority will hinge on lien validity and collateral tracing. If double-pledging is proven, expect litigation over who owns which receivable or inventory proceeds.

Weakened Customer Traffic

- Average daily customer count hovered between 2,500 and 5,000, below earlier years' benchmarks.

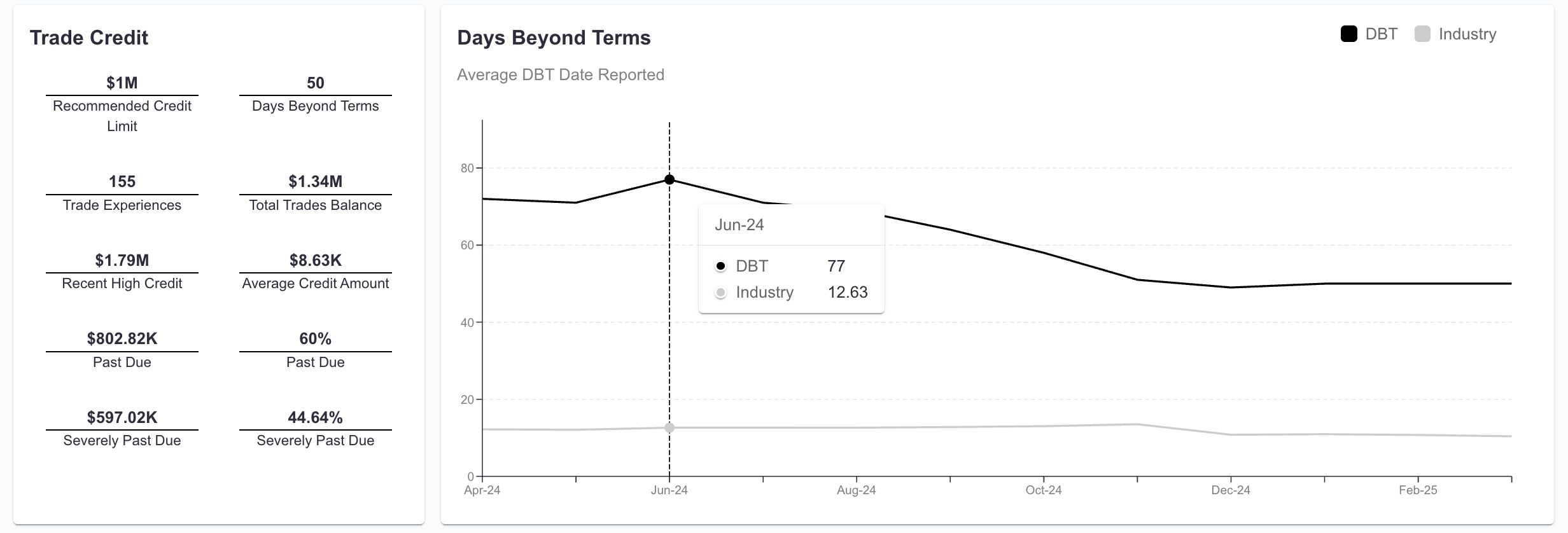

Credit Deterioration

- Days Beyond Terms (DBT) climbed as high as 75 days in 2024 before modestly improving to 50 days in early 2025, still far worse than the industry average.

- 60% of Bertucci’s trade balances were past due, with nearly 45% severely delinquent.

- Trade balances outstanding grew heavier in the 91+ days overdue category, showing strained liquidity.

Headcount Erosion

- After peaking near 950 employees in 2015, Bertucci’s workforce steadily declined year over year.

- As of early 2025, headcount was below 400 employees, a 2.9% drop over the last 12 months alone.

Payment Behavior Stress

- Outstanding trade lines showed a growing share of invoices slipping past 91+ days overdue.

- Despite a $1M recommended credit limit, Bertucci’s outstanding and aging trade behavior told a story of mounting pressure that was unsustainable.

Bertucci’s financial health was declining across every key dimension long before bankruptcy became public.

Lessons for Credit and Risk Professionals

Bertucci’s offers an important reminder: A slow decline can be just as fatal as a sudden collapse.

Multiple bankruptcies are a major risk flag. Emerging from bankruptcy without structural change often leads to repeated failures.

Revenue rebounds must be sustainable. A brief spike in 2022 did not reflect real recovery. Fundamental problems remained unaddressed.

Worsening payment behavior is an early alarm. Ballooning DBT, a rising share of severely overdue invoices, and shrinking employee counts were clear signs of deep trouble.

Adaptation is non-negotiable. Businesses that fail to meet shifting customer expectations eventually lose relevance, no matter how strong they once were.

Credit Pulse: Catch the Early Signals

At Credit Pulse, we track early signals that traditional reports miss. From falling headcounts to deteriorating payment behavior, we identify risk before it becomes a crisis.

Bertucci’s third bankruptcy was not surprising for those who were watching the right indicators. You can stay ahead of situations like this too — before they reach your balance sheet.

Want to learn how? Let's talk.

Transform your credit process today.

Meet with our team or try us free for 30 days.